Thomson Reserve Review 2026: The Cheapest RCR Land of the 2026 Cohort

Updated 1 June 2026.

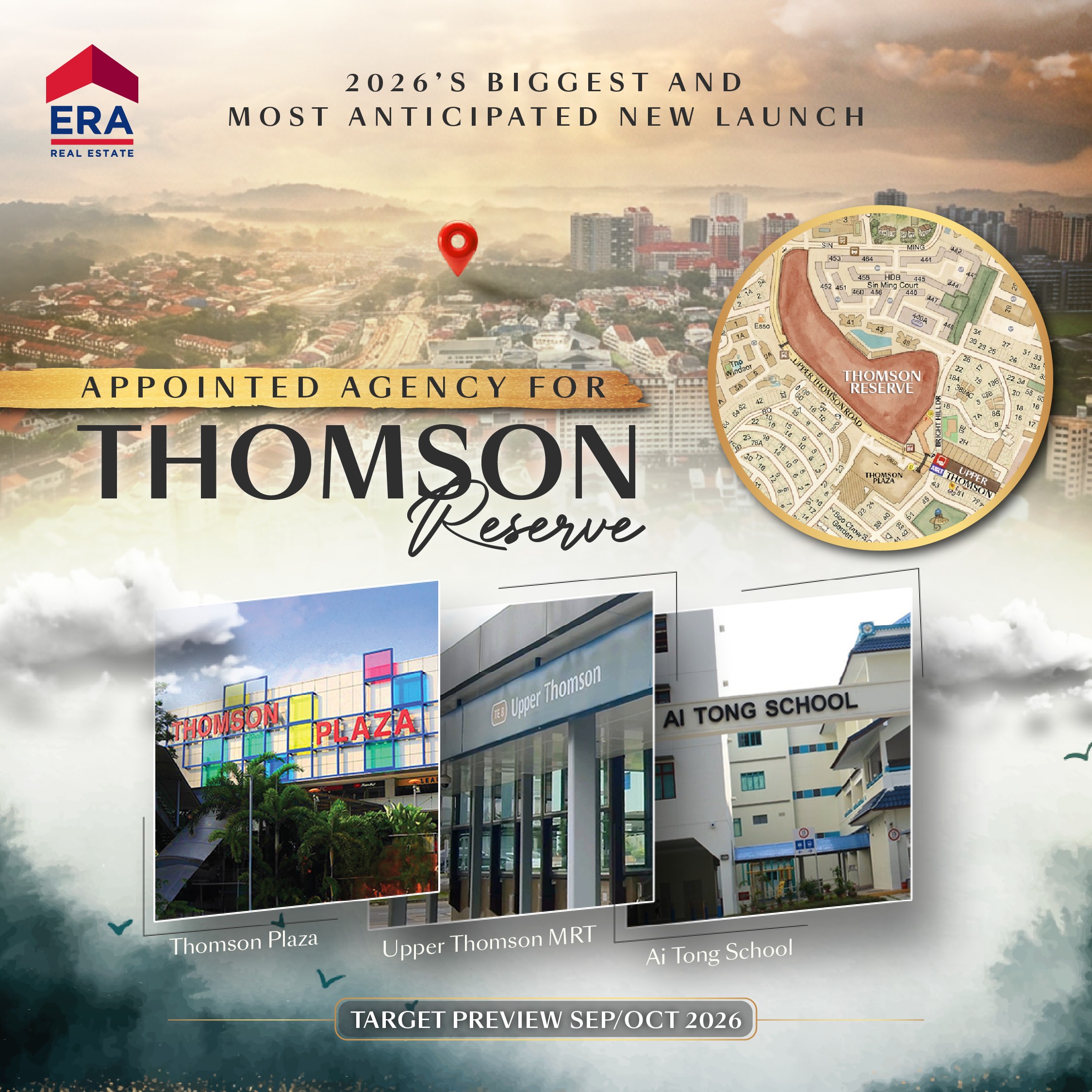

Status: pre-preview. Target preview window is Sep/Oct 2026 per current marketing. Pricing is not officially released yet. I will re-review this within one week of official price launch.

Intro

Thomson Reserve sits on the old Thomson View site at Bright Hill Drive. UOL, Singapore Land, and CapitaLand bought it en-bloc in November 2024 for $810 million. After the lease upgrading premium for a fresh 99-year tenure and land betterment charges, the effective land cost is $1,178 PSF PPR.

That number is the headline. It is the cheapest RCR land of any 2026 launch. It is also cheaper than every OCR plot tendered in 2025 and 2026 (Lentor Central $1,278, Chuan Grove $1,331 to $1,376, Vela Bay $1,388). The pricing question is whether the three-developer consortium passes that cushion to buyers or banks it as margin.

My short call, by buyer profile. HDB upgrader family from Bishan or AMK with an Ai Tong P1 target and a 7 to 10 year hold: BUY if priced at the low end of the expected $2,400 to $2,550 PSF band. Dual-income TEL plus CRL commuter couple: the 2BR Premium at $1.62M to $1.67M is the right entry. Thomson corridor rightsizer (Sky@eleven, Thomson Three owner): this is the cleanest fit on the page, BUY 3BR or 4BR. Yield investor: RCR net yield 2.4% to 2.6% is precinct-norm, not best-in-class. Short-hold flipper under 3 years: pass, 6 year wait to TOP plus megaproject tail. Full ALPHA breakdown below.

If you want me to run the math on a specific unit, just WhatsApp me. No pitch, no follow-up spam.

About Thomson: mature precinct meets en-bloc reset

Thomson is not a transformation story. It is one of Singapore's most established middle-class private corridors. Sky@eleven (2007, freehold), Thomson Grand (2013), Thomson Three (2016), Thomson Impressions (2018), and the smaller estates around Bishan and Marymount have been trading steadily for over a decade. TEL Phase 4 went live in 2024 and gave the area a second wind on connectivity. The next phase is en-bloc.

The Thomson View en-bloc that became Thomson Reserve is the headline 2024 deal in this corridor. But it sits inside a wider en-bloc wave that has been quietly resetting Thomson land. Five collective sale attempts at Thomson View over 17 years finally cleared in November 2024 after the reserve price was cut from $918 million to $808 million. UOL and CapitaLand exercised their call option at $810 million on 25 November 2024. Singapore Land Group came in shortly after as the third partner. It was the second-biggest en-bloc deal of 2024 after Chuan Park at $890 million.

Three reasons the land basis ended up where it did:

- The reserve price was reset. $110 million came off the asking. Owners chose certainty over holdout after almost two decades of failed attempts.

- Three-way JV de-risks the megaproject. 1,268 units is too big for one developer to absorb cleanly. Splitting risk across three blue chips made aggressive bidding possible.

- Fresh 99-year lease, premium paid upfront. The $1,178 PSF PPR figure already includes the cost to refresh the tenure. Buyers get a brand new 99-year lease at that headline number.

📸 IMAGE 2: 2026 launch cohort land cost comparison chart (highest priority chart, make this the cleanest)

Designed paired-bar chart (Canva or Datawrapper). 1600 x 900 px. Sort ascending, highlight Thomson Reserve in gold.

Data points: Lentor Gardens (OCR D26) $920. Thomson Reserve (RCR D20) $1,178 (gold). Lentor Central (OCR D26) $1,278. Telok Blangah (RCR) $1,326. Bedok Rise (OCR) $1,330. Chuan Grove 2 (OCR) $1,331. Dorsett Road (RCR) $1,338. Chuan Grove 1 (OCR) $1,376. Vela Bay (OCR) $1,388. Dunearn House (RCR) $1,410. Kallang Close (RCR) $1,415. Holland Link (RCR) $1,432. Tanjong Rhu (RCR) $1,455. Dover Drive (RCR) $1,556. Dunearn Road (RCR) $1,625. Bukit Timah (RCR) $1,820.

Caption: "Thomson Reserve at $1,178 PSF PPR. Up to 54% below RCR peers and 18% below OCR comparables. Cheapest 2026 launch land outside the Lentor cycle."

Replace with

There are two ways to read the chart. Against RCR peers, Thomson Reserve is up to 54% cheaper. Bukit Timah at $1,820 is the extreme. Even mid-pack RCR (Holland Link, Kallang Close, Tanjong Rhu) sits 20% to 24% higher. That is a real anomaly.

The more interesting comparison is against OCR. RCR land is normally 20% to 35% more expensive than OCR by location pricing convention. Thomson Reserve breaks that convention. Lentor Central OCR went for $1,278, Chuan Grove OCR for $1,331 to $1,376, Vela Bay OCR for $1,388. All of those are higher than Thomson Reserve's RCR plot. That is the mispricing thesis driving the whole review.

Sources: EdgeProp UOL-CapitaLand call option, EdgeProp biggest en-bloc deal 2024, official project information hub, current developer marketing.

Project overview

| Item | Detail |

|---|---|

| Developer | UOL Group, Singapore Land Group, CapitaLand Development (3-way JV) |

| Tenure | Fresh 99-year leasehold (lease premium paid as part of the en-bloc) |

| Address | Bright Hill Drive, District 20, RCR |

| Total units | 1,268 (estimated) |

| Site area | 540,434 sqft (around 5 hectares) |

| Block configuration | 4 blocks of 21 storeys plus 2 blocks of 30 storeys (TBC) |

| Unit types | 9 types: 1BR+Study, 2BR, 2BR Premium, 2BR Premium+Study, 3BR, 3BR Premium, 3BR Premium+Study, 4BR, 4BR Premium (per-type counts at preview) |

| Estimated sizes | 506 · 581 · 667 · 732 · 818 · 915 · 1,033 · 1,173 · 1,238 sqft (1BR+S through 4BR Premium) |

| Land cost | $810M total, $1,178 PSF PPR (after LBC and lease premium) |

| Plot ratio | Around 2.8 |

| Density per unit | About 426 sqft, lowest of any 2020s mega launch |

| Preview | Sep/Oct 2026 target |

| Showflat | Serangoon Crescent (offsite) |

| TOP | Around 2032 (TBC) |

| Nature buffer | MacRitchie Reservoir on the south boundary |

Developer track record: UOL + Singapore Land + CapitaLand

Three SGX-listed blue chips. Each brings something different.

UOL Group is the lead developer brand. Recent reference points: Avenue South Residence (D03 RCR, 1,074 units, sold out), Watergardens at Canberra (D27 OCR, 448 units, sold out). UOL's finish at handover sits in the upper-mainstream tier (better than CDL volume product, just below Wing Tai or Far East flagship grade). Their sell-through history at scale is one of the most reliable in Singapore.

Singapore Land Group brings deep Thomson corridor history. They have held and developed assets in this area for decades. Smaller residential volume but consistent finish quality, plus freehold portfolio depth that signals patience and pricing discipline.

CapitaLand Development is the third leg. Recent local product: One Pearl Bank (D03 RCR, 774 units, sold out), Sengkang Grand Residences (D19 OCR), Canninghill Piers (D06 CCR).

Their recent launch performance, with cheques collected against units sold, tells you what to expect at preview:

| Project | Developer | Cheques | Launch sales | Avg PSF |

|---|---|---|---|---|

| Skye at Holland | UOL + CapitaLand | 2,101 | 656 / 666 (99%) | $2,953 |

| Pinery Residences | CapitaLand | 1,290 | 544 / 588 (92%) | $2,546 |

| Parktown Residence | UOL + CapitaLand | 2,315 | 1,041 / 1,193 (87%) | $2,360 |

What this tells me about pricing, and it cuts both ways. The good news for buyers: this consortium has a documented habit of leaving value on the table. Parktown Residence collected 2,315 cheques against 1,193 units, a 2-to-1 oversubscription, and still held its price through the entire booking day without raising it. Skye at Holland cleared 99% despite a higher land cost, at an eventual average about $100 PSF below a directly comparable project. When you want a developer to get land at a good price and pass some through, it is them.

The caution: three blue chips with strong brand equity do not race each other to the bottom either. They price with discipline, not desperation. Some of the land cushion flows to buyers, a meaningful share gets kept as margin. Do not expect a fire sale, expect a fair one.

Site technicals

Site area 540,434 sqft, plot ratio around 2.8. Six blocks total: four at 21 storeys, two at 30 storeys. GFA on 540,434 sqft at GPR 2.8 implies a maximum permissible GFA around 1,513,000 sqft, consistent with the 1,268-unit count and the block configuration.

| Region | Typical residential GPR |

|---|---|

| OCR suburban | 1.4 to 2.8 |

| OCR near MRT | 2.5 to 3.5 |

| RCR city-fringe (Thomson Reserve) | 2.8 to 3.5 |

| CCR | 4.0 to 5.6 |

Thomson Reserve sits at the lower end of typical RCR density. The 6-block configuration with two 30-storey towers and four 21-storey blocks is unusually generous spacing for this scale. The two 30-storey towers carry the view premium. The four 21-storey blocks fill the mid-rise tier and offer lower entry quantum.

Lowest density in the 2020s mega launch cohort

| Development | Units | Land size (sqft) | Sqft per unit |

|---|---|---|---|

| Treasure at Tampines | 2,203 | 648,000 | 294 |

| Grand Dunman | 1,008 | 271,000 | 269 |

| Jadescape | 1,206 | 409,000 | 339 |

| Normanton Park | 1,862 | 661,000 | 355 |

| Thomson Reserve | 1,268 | 540,434 | 426 |

At 426 sqft of land per unit, Thomson Reserve gives 20% to 45% more land per resident than the recent megaproject reference set. That matters at this scale. Pool overcrowding, lift congestion at peak, gym waitlists, shared driveway pinch points all scale with sqft per unit. A 1,268-unit project at 426 sqft per unit lives differently from one at 350.

Combined with 80% plus landscaping retention on the developable footprint, this is the rare megaproject that can credibly claim mega scale without mega density downside.

Surrounding boundaries

- North: Sin Ming Avenue, with Sin Ming Court HDB precinct beyond. Low to mid-rise, stable.

- South: MacRitchie Reservoir Park. URA protected. Permanent low-rise green buffer.

- East: Bright Hill Drive frontage and existing Thomson corridor private condos (Thomson Three, Thomson Impression).

- West: Upper Thomson Road with landed pockets behind.

The MacRitchie buffer on the south is the standout site feature. Permanent protected green frontage next to an MRT interchange is genuinely rare in Singapore private residential. Closest comparable is Caldecott Hill or Marymount, where the same characteristic has supported premium pricing for over a decade.

Facilities & site plan

The site plan shows 14 facility types numbered on the plan:

- Tennis Court

- Multi-Purpose Court

- Clubhouse

- BBQ Pavilion

- Swimming Pool

- Kids Pool / Play Zone

- Bin Centre (basement)

- Electrical Substation & Transformer Rooms (basement)

- Genset

- Gym

- Pickup and Drop Off

- Pavilion

- Playground

- Fitness Corner

Site plan boundaries: Sin Ming Avenue (north), Bright Hill Drive (east), Upper Thomson Road (west). The side gate sits on the south-east edge facing Upper Thomson MRT entrance.

What to walk at the show flat:

- Side gate connectivity to Upper Thomson MRT. Actual walking time door to platform. Sheltered or not.

- MacRitchie boundary access. Is there a direct pedestrian gate to the park, or do you walk around?

- Block-to-block spacing. At 6 blocks the worst stacks face other Thomson Reserve blocks.

- Childcare or ECDC inclusion if any.

- Drop-off and carpark capacity at 1,268 units.

One thing to flag on the "integrated lifestyle" claim. Thomson Reserve does not have on-site retail like Lentor Modern or Sengkang Grand. What it has is a clean MRT linkway to Thomson Plaza (a 1979 mall with FairPrice, F&B, services). It is best-in-class walkable convenience to nearby retail. It is not on-site integrated retail. Treat it as the former, not the latter.

Access: MRT, schools, lifestyle

📸 IMAGE 3: Upper Thomson MRT (TE8) station entrance (placeholder)

Real photograph. 1600 x 900 px landscape. Take it yourself (1-minute walk from Thomson Reserve side gate).

Caption: "Upper Thomson MRT (TE8). 1-minute walk via side gate. TEL to Orchard in 5 stops."

Replace with

MRT and dual-line catchment

Side gate access to Upper Thomson MRT (TE8) on the Thomson East Coast Line. 1-minute walk per the published site plan. From TE8: 5 stops to Orchard, 9 to 11 stops to CBD or Marina Bay.

Bright Hill MRT (TE7) is also walkable, about 8 to 10 minutes on foot. This is the more important station for the long view. Bright Hill becomes a Cross Island Line plus TEL interchange when CRL Phase 1 opens in 2030, with Phase 2 extending in 2032. Per LTA CRL planning data:

- Hougang: 40 minutes becomes 20 minutes

- Pasir Ris East: 80 minutes becomes 30 minutes

- 1 station to Turf City MRT

Single-line catchment becoming dual-line is historically one of the strongest mid-cycle resale uplift drivers in Singapore. The 2030 CRL timing aligns with the 2032 TOP, which means the dual-line effect activates around when owners take possession. This is the access engine for the whole investment thesis.

Bus: 10 routes from Upper Thomson Station Exit 2 (132, 162, 163, 165, 166, 167, 410W, 52, 855, 980).

Drive times: Orchard 10 minutes, Novena 8 minutes, CBD 15 minutes off peak.

Schools

📸 IMAGE 4: Ai Tong School (placeholder)

Real photograph. 1600 x 900 px. Take it yourself or use Wikipedia CC photo.

Caption: "Ai Tong School within the 1 km P1 priority ring."

Replace with

Ai Tong School sits within the 1 km P1 priority ring. This is the catchment anchor. One thing to know: Ai Tong has gone to Phase 2C balloting for several recent years per MOE data. Being inside the 1 km radius improves your odds, it does not guarantee a seat. Plan for the ballot, not the certainty.

Within 1 to 3 km: Catholic High School, CHIJ St Nicholas Girls' School, Raffles Institution, Raffles Girls' Secondary, Marymount Convent, Bishan Park Secondary. The school axis here is one of the strongest in the RCR.

Daily life

📸 IMAGE 5: MacRitchie Reservoir Park (placeholder)

Real photograph. Caption: "MacRitchie Reservoir Park on Thomson Reserve's south boundary."

Replace with

MacRitchie Reservoir Park is the south boundary of the site. Protected green. Free hiking. Thomson Plaza is across the MRT linkway: FairPrice, F&B, daily run stuff. Bishan Junction 8 is a 5-minute drive. Existing neighbour condos in the immediate Thomson corridor: Thomson Three (445 units, TOP 2016), Thomson Impressions (288, TOP 2018), Bishan Point (164, TOP 2005), The Windsor (159, TOP 1988).

If you want to compare Thomson Reserve against the OCR alternative on the same TEL line, read my Lentor Gardens Residences review. Cheaper land, smaller scale, different cycle position.

Layout: reading the unit mix

Per-type unit counts and stack assignments release at the Sep/Oct preview. The full type ladder and indicative entry pricing are now circulating in the market. These prices are estimates based on current comparable sizing, not the developer's official price list, so treat them as a guide to the shape of the launch rather than a quote.

| Unit type | Est. size (sqft) | Indicative from | Implied PSF |

|---|---|---|---|

| 1BR + Study | 506 | $1.2M | ~$2,370 |

| 2BR | 581 | $1.4M | ~$2,410 |

| 2BR Premium | 667 | $1.7M | ~$2,550 |

| 2BR Premium + Study | 732 | $1.7M | ~$2,320 |

| 3BR | 818 | $2.1M | ~$2,570 |

| 3BR Premium | 915 | $2.3M | ~$2,510 |

| 3BR Premium + Study | 1,033 | $2.3M | ~$2,230 |

| 4BR | 1,173 | $2.9M | ~$2,470 |

| 4BR Premium | 1,238 | $3.1M | ~$2,500 |

Nine types from a 506 sqft 1BR+study up to a 1,238 sqft 4BR Premium. The implied PSF clusters at $2,300 to $2,570, which is the entire pricing story: it lands at or below where the resale market already sits (see Premium below).

Who each unit type fits

1BR + Study, around 506 sqft, from about $1.2M. The entry ticket. Single professionals and pure-rental investors. At about $2,370 PSF this is the lowest-quantum way into a fresh 99-year RCR unit one minute from the MRT. Tenant demand from Thomson-corridor professionals and CBD commuters via TEL.

2BR range, 581 to 732 sqft, from about $1.4M to $1.7M. The volume tier. The plain 581 sqft 2BR from about $1.4M is the sharpest entry: Jadescape's 646 sqft 2BR units trade at $2,260 to $2,323 PSF in recent caveats, so a Thomson Reserve 2BR at roughly $2,410 PSF launch is only a few percent above 8-year-old Jadescape resale. The 667 sqft Premium and 732 sqft Premium+Study widen the tenant and resale pool with a second bathroom and a study, and the 732 sqft variant actually carries a lower PSF, which makes it the value pick of the tier.

3BR range, 818 to 1,033 sqft, from about $2.1M to $2.3M. The family sweet spot and the segment Bishan, AMK, and Yishun HDB upgraders compete for. Comparable 900-plus sqft 3BRs at Jadescape, Lentor Central, and AMO Residences trade at $2,432 to $2,610 PSF, so the 915 sqft 3BR Premium at roughly $2,510 PSF sits inside the live resale range. The 1,033 sqft Premium+Study at about $2.3M is the standout on PSF (~$2,230), the layout a 5-room HDB upgrader should hunt for.

4BR range, 1,173 to 1,238 sqft, from about $2.9M to $3.1M. Family of four or five, or a downsizer from landed. About $2.9M for the 1,173 sqft 4BR puts it in upgrader-from-5-room-HDB territory. The structural buyer pool: about 66,509 HDB flats in the Bishan and AMK Planning Area per URA Planning Area data.

Megaproject absorption: realistic vs marketing

1,268 units is a lot to clear at preview. Reference points from recent megaprojects:

- Avenue South Residence (UOL, 1,074 units, D03): cleared in around 12 months at strong absorption pace.

- Normanton Park (Kingsford, 1,862 units, D05): hit 70% at preview, took 18 months to clear long tail.

- Parktown Residence (UOL plus CapitaLand): 87% launch-day absorption, 1,041 units moved on day one against 2,315 cheques collected.

Realistic Thomson Reserve absorption profile, with consortium track record plus cheapest-cohort land plus strong catchment:

- Preview weekend: 35% to 55% (440 to 700 units of 1,268)

- First 90 days: 65% to 80% (820 to 1,015 units)

- Long tail: 20% to 35% (250 to 450 units) clearing over 12 to 18 months

Some salesforce material in circulation positions a "1,000-plus units in launch weekend" scenario, which would be about 80% absorption in two days. That would set a new RCR record. Possible given the consortium's track record, but not the realistic base case. 50% to 65% launch weekend is more honest and still strong.

How supply-light is the immediate area?

The Thomson Reserve enclave is genuinely supply-constrained today. Within a 500m radius:

| Existing condo | Units | TOP |

|---|---|---|

| Thomson Three | 445 | 2016 |

| Thomson Impressions | 288 | 2018 |

| Bishan Point | 164 | 2005 |

| The Windsor | 159 | 1988 |

| Country Grandeur | 68 | TBC |

| Three 11 | 65 | 2015 |

| Country Esquire | 60 | 1992 |

| Thomson Plaza | 20 | 1979 |

| Total | 1,269 |

For comparison, River Green's 500m radius contains 9,544 condo units. Thomson Reserve's enclave is about 13% as dense in private residential. Adding Thomson Reserve's 1,268 roughly doubles the local stock but still leaves the area less dense than typical RCR locations. Good for resale liquidity.

Floor plans (pending release at Sep/Oct 2026 preview)

What is known today: total unit count (1,268), the 6-block configuration (4 by 21-storey plus 2 by 30-storey), side-gate access to Upper Thomson MRT, and the nine-type unit ladder with indicative sizes and entry prices (in the Layout section above).

What is NOT yet public, releases at the Sep/Oct 2026 preview:

- Per-unit-type unit counts (how many of each of the nine types)

- Stack assignments per block

- Floor ranges per stack

- Bedroom dimensions and the actual floor plan drawings

- Wet or dry kitchen, service yard, household shelter inclusions

- Exact stack orientation

- Which blocks front MacRitchie versus which face internal podium

I will re-issue this review within a week of the preview with the full stack-level analysis.

If Thomson Reserve is on your shortlist and you want the floor-plan-level read on day one, drop me a message. I'll WhatsApp you the breakdown as soon as the brochure drops.

Which stack should I pick?

Full stack analysis releases post-preview. Directional logic for now:

| Direction | What you likely see | Best for |

|---|---|---|

| South | MacRitchie Reservoir Park (protected) | Best view profile. Permanent nature buffer, lowest noise |

| East | Bright Hill Drive plus existing Thomson Three / Impression | Stable mid-floor view, road noise on lower floors |

| North | Sin Ming Avenue plus Sin Ming Court HDB | Mid-rise stable view, urban distance |

| West | Upper Thomson Road plus landed pockets | Acceptable, lower floors may have road exposure |

Primary call: south-facing upper floors in the two 30-storey blocks for the MacRitchie buffer view. This is the single highest-value facing on the site. Among the 6 blocks, internal-courtyard-facing stacks are the standard "value entry" picks (lower quantum, fewer view premiums priced in).

Confirm at the show flat the exact block orientation and which stacks have direct MacRitchie sightlines without intervening blocks.

[IMAGE 6: Stack orientation matrix. Defer until preview confirms block placement.]

Premium: is the expected $2,400 to $2,550 PSF band defensible?

This is where the land cost advantage meets market pricing.

Land cost is $1,178 PSF PPR. RCR multiplier rule of thumb (1.9 to 2.4 times land cost, per ALPHA playbook, rule of thumb not a sourced formula) implies expected launch PSF of $2,238 to $2,827. The indicated $2,400 to $2,550 band per current developer marketing sits in the lower-middle of that range at a multiplier around 2.04 to 2.16 times. Not stretching. Not giving it away either.

Versus 2025 RCR launches by the same consortium

| Project | Launch PSF | Outcome |

|---|---|---|

| Skye at Holland (2025) | $2,953 | 99% sold |

| Pinery Residences (2025) | $2,546 | 92.5% sold |

| LyndenWoods (2025) | $2,450 | 94.5% sold |

| Parktown Residence (2025) | $2,360 | 87% sold launch day (2,315 cheques) |

| Thomson Reserve (2026, indicated) | $2,400 to $2,550 | TBC |

Versus current resale along the Thomson-East Coast Line

Recent transactions on the newest TEL resale developments, shown non-harmonised and harmonised. The harmonised figure adjusts older strata areas to today's GFA rules, so it is the apples-to-apples comparison against a 2026 launch:

| Project | TOP | Avg PSF 2026 (non-harm / harm) | Recent 2BR | Recent 3BR |

|---|---|---|---|---|

| Thomson Three | 2016 | $2,204 / $2,336 | $1,585,000 | $2,640,000 |

| Lentor Modern | 2026 | $2,404 / $2,548 | $1,860,000 | $2,675,000 |

| Sky@Eleven | 2010 | $2,430 / $2,576 | n/a | $5,750,000 |

| AMO Residence | 2026 | $2,549 / $2,702 | $1,828,000 | $3,020,000 |

What this tells you. On a harmonised basis, the newest TEL resale sits at $2,336 to $2,702 PSF. Thomson Reserve's indicative launch, roughly $2,300 to $2,570 PSF, lands at or below that range while being brand new with a fresh 99-year lease. The most recent 2BR resales at AMO Residence ($1,828,000) and Lentor Modern ($1,860,000) bracket Thomson Reserve's indicative 2BR entry from about $1.4M. That is the "new launch at resale price" thesis, and unlike most launch pitches it is backed by live transactions rather than a brochure.

Versus recent RCR launch entry prices

The sharper comparison is against what buyers are paying to enter other RCR launches near an MRT right now. Indicative Thomson Reserve entry quanta against recent RCR starting prices:

| Project | 2BR from | 3BR from | 4BR from |

|---|---|---|---|

| Thomson Reserve (indicative) | ~$1.4M | ~$2.1M | ~$2.9M |

| One Marina Gardens | $1.88M | $2.56M | $4.77M |

| Union Square Residences | $1.89M | $2.61M | $3.18M |

| 8@BT | $1.89M | $2.82M | $3.65M |

| Terra Hill | $1.94M | $2.49M | $3.53M |

| Promenade Peak | $2.06M | $3.21M | $4.63M |

| Zyon Grand | $2.31M | $2.76M | $4.71M |

Across all three bedroom counts, Thomson Reserve's indicative entry undercuts the recent RCR field. The honest caveat: part of that gap is smaller entry sizes, the 581 sqft 2BR is more compact than some comps, so compare PSF as well as quantum. But even on PSF, roughly $2,300 to $2,570, Thomson Reserve sits at the bottom of the RCR pack. This is the "RCR at OCR price" argument, and it is the single strongest thing the project has going for it.

My read: at the low end this is a genuine value entry for the precinct. At the top of the indicative range it is a standard RCR market-price call. The Sep/Oct preview tells us which.

📸 IMAGE 7: Pricing scenario card (placeholder)

Designed three-tier card (Canva), 1600 x 900 px, three columns.

Column 1 (green): "$2,400 to $2,450 PSF" + "Consortium prices to land cushion advantage". Column 2 (gold): "$2,475 to $2,525 PSF" + "Consortium prices to indicated range". Column 3 (red): "$2,550 plus PSF" + "Consortium banks the cushion".

Caption: "Three pricing scenarios. Watch the Sep/Oct preview to see which lane the JV runs."

Replace with

Monthly mortgage on a 3BR. 3BR around 915 sqft at $2,500 PSF works out to $2.29M. At 75% LTV ($1.72M loan), 25-year tenure, 1.7% fixed Y1 to Y2 (typical April 2026 package), monthly mortgage is about $7,030. Total upfront (downpayment plus BSD plus legal) about $650K.

Verdict on Premium. Land cost provides cushion. The consortium does not have to pass it all to buyers. Watch the preview pricing as the earliest signal of which lane they run.

Want to check how much ABSD or BSD you'd pay on top? Use the ABSD Calculator to get your exact number in seconds.

Quantum & cashflow: scenario table (pre-launch)

Three scenarios. Assumes 75% LTV, 25-year tenure, 1.7% fixed Y1 to Y2, Singapore Citizen 1st property (no ABSD).

Low-end scenario, $2,400 to $2,450 PSF:

| Unit | Size (sqft) | PSF | Price | Upfront | Monthly |

|---|---|---|---|---|---|

| 2BR | 581 | $2,400 | $1.39M | About $395K | About $4,290 |

| 2BR Premium | 667 | $2,425 | $1.62M | About $459K | About $4,970 |

| 3BR | 915 | $2,450 | $2.24M | About $634K | About $6,870 |

| 4BR | 1,173 | $2,450 | $2.87M | About $813K | About $8,810 |

Mid scenario (indicated band), $2,475 to $2,525 PSF:

| Unit | Size (sqft) | PSF | Price | Upfront | Monthly |

|---|---|---|---|---|---|

| 2BR | 581 | $2,475 | $1.44M | About $408K | About $4,420 |

| 2BR Premium | 667 | $2,500 | $1.67M | About $472K | About $5,120 |

| 3BR | 915 | $2,513 | $2.30M | About $652K | About $7,060 |

| 4BR | 1,173 | $2,475 | $2.90M | About $823K | About $8,920 |

Stretch scenario, $2,550-plus PSF:

| Unit | Size (sqft) | PSF | Price | Upfront | Monthly |

|---|---|---|---|---|---|

| 2BR | 581 | $2,550 | $1.48M | About $420K | About $4,560 |

| 2BR Premium | 667 | $2,600 | $1.73M | About $491K | About $5,330 |

| 3BR | 915 | $2,600 | $2.38M | About $674K | About $7,300 |

| 4BR | 1,173 | $2,600 | $3.05M | About $865K | About $9,370 |

Not sure if the numbers work for your income? Use the Mortgage Calculator or TDSR Calculator to check your maximum loan before you commit.

Rental comps: Thomson corridor data

Data from active rentals in the immediate corridor:

| Project | 2BR rent estimate | 3BR rent estimate |

|---|---|---|

| Thomson Three | $4,200 to $5,000 / month | $6,000 to $7,500 / month |

| Thomson Impressions | $4,200 to $5,000 / month | $5,800 to $7,200 / month |

| Sky@eleven | $4,500 to $5,500 / month | $6,500 to $8,000 / month |

| Sin Ming Arc | $4,300 to $5,200 / month | $6,200 to $7,500 / month |

Calibration for Thomson Reserve at mid scenario:

- 2BR Premium at $1.67M, rented at $5,000 / month: gross yield around 3.6%, net around 2.6%.

- 3BR at $2.30M, rented at $6,800 / month: gross yield around 3.5%, net around 2.5%.

Industry research documents about 13% rental premium for true integrated-mall developments (Park Colonial $7.04 PSF versus Tre Ver $6.20 PSF is a commonly cited comparison). Thomson Reserve has MRT-linked Thomson Plaza access, not on-site integrated retail. Expect 5% to 8% of that premium to apply, not the full 13%.

Verdict for investors. RCR-norm yield, not best-in-class. Thomson Reserve competes on precinct prestige, MacRitchie buffer, dual-line MRT post-2030, and the Ai Tong plus Catholic High plus Raffles school axis. Not on yield.

Horizon: what catalyses Thomson 2026 to 2035

Thomson is a mature precinct repricing on infrastructure and scarcity. The Horizon thesis for Thomson Reserve is not "area transforms" (that phase happened a decade ago). It is "established prime corridor re-rates upward as CRL adds the second-line catchment, and Thomson Reserve absorbs as the only meaningful private launch in the immediate Bright Hill / Upper Thomson micro-precinct for the foreseeable horizon."

Both the Macro (wider corridor narrative) and Micro (plot-by-plot inside 1 km) matter. Read both.

Macro masterplan: Thomson, Bright Hill, Bishan corridor

- TEL is operational. Known good, not a future catalyst.

- Cross Island Line Phase 1 opens 2030. Bright Hill becomes the CRL plus TEL interchange. Hougang travel falls from 40 to 20 minutes. Pasir Ris East from 80 to 30 minutes. 1 station to Turf City MRT. This is the structural Horizon catalyst.

- CRL Phase 2 extends 2032. Adds further connectivity uplift. Lines up with TOP.

- MacRitchie Reservoir and Central Catchment Nature Reserve. URA-protected green belt that cannot be built over. Thomson Reserve's south frontage looks at it.

- 66,509 HDB flats in Bishan and AMK Planning Area per URA Planning Area data. Structural upgrader pool feeding the precinct through 2030 and beyond.

- No major Thomson area GLS coming. Unlike Lentor where Plot 2 is on URA's pipeline, the Bright Hill / Upper Thomson micro-precinct has no obvious next launch. Bullish for Thomson Reserve resale post-2032 because there is no Plot 2 to compete with for the rest of the decade.

Micro masterplan: what's happening inside 1 km

- No competing private launches inside 1 km through 2030.

- Bishan-AMK HDB MOP pipeline: several thousand units hitting MOP between 2026 and 2030. At a 10% upgrade rate, sustained upgrader demand.

- Thomson rightsizers: Sky@eleven (2007), Thomson Three (2016), Thomson Impressions (2018), Thomson Grand (2013) owners ageing into 55-plus and looking at fresh 99-year stock. Thomson Reserve is the natural rotation destination.

- Schools and roads: Ai Tong catchment unchanged. Bright Hill Drive and Sin Ming Avenue upgrades already done. No construction disruption other than the Thomson Reserve site itself through 2032.

Buyer pool at exit (2033 to 2036)

When a Thomson Reserve unit goes to resale, the likely buyers:

- HDB upgrader family from Bishan or AMK, Ai Tong P1 target, 3BR budget $2.5M to $3.0M

- Dual-income TEL plus CRL commuter couple, 2BR Premium budget $1.8M to $2.2M

- Thomson corridor rightsizer (Sky@eleven, Thomson Three owner), 3BR or 4BR budget $2.5M to $3.5M

- Second-home investor wanting RCR rental, 2BR budget $1.6M to $2.0M

Exit liquidity: strong. RCR D20, MacRitchie buffer, CRL interchange, no immediate competing launch, supply-constrained enclave. Better positioned than Lentor Gardens' exit liquidity profile.

Upgrading from HDB? Read the HDB to Condo Upgrade Guide for the timeline, CPF refund rules, and cost breakdown.

Horizon bottom line

Buyers are betting that CRL 2030 plus CRL 2032 plus MacRitchie scarcity plus no Plot 2 competition plus the structural 66k HDB upgrader pool combine to drive resale uplift from launch through to the 2033 to 2036 exit window. For a 7 to 10 year hold this is credible because multiple catalysts genuinely align in the same time band. Under 5 years the consortium's pricing discipline (margin-anchored, not give-it-away) means flip economics are tough. Plan for 7-plus years.

Asymmetry: honest upside and downside

Upside paths:

- Consortium prices at the low end ($2,400 to $2,450), Thomson Reserve absorbs 60% to 80% at launch weekend, early buyers see 8% to 15% resale uplift between TOP 2032 and full CRL maturation 2033 to 2034.

- CRL Phase 1 opens on schedule 2030, Bright Hill catchment re-rates faster than expected, dual-line uplift compounds on top of the launch-basis cushion.

- Thomson corridor rightsizer flow accelerates as Sky@eleven, Thomson Three, Thomson Impression owners age into 55-plus and seek fresh 99-year stock. 3BR Premium and 4BR scarce, resale plus 15% to 20%.

- Megaproject becomes the area's brand anchor. Facility breadth plus density advantage compound into a "Thomson Reserve premium" similar to how Park Colonial commands rental premium over Tre Ver.

Downside paths:

- Consortium prices to RCR margin ($2,550-plus), absorption stalls at 50% to 60%, the 1,268-unit overhang sits on the market through 2027 to 2028. Long tail creates secondary-market price discovery noise.

- CRL Phase 1 delays 12 to 18 months. The 2030 catalyst slides to 2031 or 2032, eroding resale uplift timing for 2033 exits.

- Three-way JV friction emerges on pricing or finishing. Brand finish at TOP does not match the consortium's recent track record.

- Megaproject scale means even strong absorption leaves a long tail. Last 15% to 25% of units take 18-plus months to clear, depressing secondary pricing during that window.

- Bishan and AMK HDB upgrader demand softens if MOP-era flat values cool. The structural buyer pool thesis depends on HDB equity holding up.

Numbers game for a 3BR around 915 sqft at $2.30M (mid scenario), 7-year hold:

| Scenario | Annual appreciation | Exit price | Net gain after BSD, interest, holding costs |

|---|---|---|---|

| Base (Thomson re-rates steady) | 2.5% | $2.73M | About $200K |

| Bull (CRL plus scarcity plus rightsizer demand compounds) | 5.0% | $3.24M | About $620K |

| Bear (megaproject overhang plus CRL delay) | -1.5% | $2.07M | About minus $300K before rental offset |

Risk of permanent capital loss: lower than Lentor Gardens. Better developer pedigree, no Plot 2 competition, dual-line MRT post-2030, more defensible buyer pool. Exit timing detail below.

Strategic exit timeline: matching catalysts to years

Years 1 to 4 (2026 to 2029): Accumulation and construction

- Sep/Oct 2026: VVIP or preview pricing locked in. Progressive Payment Scheme keeps initial cash outlay manageable.

- 2027 to 2029: Construction underway. North-South Corridor (NSC) 8.8 km viaduct completing in this window, improves road connectivity to city centre.

- 2028: 4-year mark since en-bloc. Secondary market in Thomson corridor resale starts informing pricing on long-tail primary units.

Years 4 to 6 (2030 to 2032): CRL inflection and TOP

- 2030: CRL Phase 1 opens. Bright Hill becomes interchange. Highest-impact catalyst on the timeline.

- SSD 4-year window: holders who bought at 2026 launch are SSD-clear by 2030. Secondary liquidity opens before TOP, which is unusual and bullish.

- 2032: TOP. Owners take possession. Rental market activates.

- 2032: CRL Phase 2 extends. Additional connectivity uplift aligning with TOP.

Years 6 to 10 (2032 to 2036): Strategic exit window

- 2032 to 2033: TOP plus early rental market.

- 2033 to 2034: Full CRL Phase 1 plus 2 maturation effects priced in.

- 2034 to 2036: Strategic exit window. HDB upgraders from 2020s-era BTOs hit MOP, Thomson rightsizer wave continues, no Plot 2 competition shows up in resale liquidity.

My call: target exit Year 7 to 10 post-launch (2033 to 2036) to capture the full CRL plus Bright Hill interchange repricing plus rightsizer demand stack. Holders who exit at TOP (2032) may miss the second leg. The structural exit timeline is 2 years longer than Lentor Gardens because TOP is 2 years later (2032 versus 2030).

Bear-case catalyst risk: if CRL Phase 1 delays past 2031, or if JV finishing at TOP draws complaints, the 2033 to 2036 window can underperform. Plan an additional 12 to 18 months of buffer cash beyond mortgage runway.

Verdict by buyer profile

| Profile | Call | Why |

|---|---|---|

| HDB upgrader family, Ai Tong P1 target, 7 to 10 yr hold | BUY (3BR, if priced $2,400 to $2,500 PSF) | Catchment plus CRL 2030 plus MacRitchie buffer plus UOL brand. Skip stretch scenario. |

| Dual-income TEL plus CRL commuter couple | BUY (2BR Premium) at low to mid scenario | $1.62M to $1.67M entry fits. If JV stretches to $2,600-plus, switch to Thomson Three or Sin Ming Arc resale. |

| Thomson corridor rightsizer (Sky@eleven, Thomson Three) | BUY (3BR to 4BR) | Fresh 99-year plus same catchment plus CRL upgrade plus density advantage. Cleanest fit on the page. |

| Yield-focused investor | PASS | RCR net yield 2.4% to 2.6% is not the play. OCR resale (Treasure at Tampines) gives 3.5% plus net. |

| Long-hold, tenure-conscious | CONSIDER Marymount freehold or nearby landed | Thomson Reserve is 99-year (fresh). No tenure step-up vs other 99-year RCR alternatives. |

| Short-hold flipper (under 3 years) | PASS | 6 years to TOP. Megaproject tail. SSD plus thin flip pool. |

| First-time SC buyer, sub $1.5M budget | CONSIDER 2BR at low scenario only | At $1.39M, 581 sqft 2BR works. Stretch scenario fails the budget. OCR alternatives may fit better. |

| Premium 4BR buyer, MacRitchie-facing | BUY at mid scenario | South-facing upper floor 4BR in the 30-storey blocks is the asymmetric pick. Queue for it at preview. |

[IMAGE 8: Verdict-by-profile card. Design as final summary graphic.]

See how I evaluate every launch with the ALPHA Framework. 5-angle method behind this review.

FAQ

Is Thomson Reserve freehold? No. Fresh 99-year leasehold (lease upgrading premium already paid as part of the $810M en-bloc deal).

What is the expected launch price? Indicative entry quanta circulating in the market (estimates based on current comparable sizing, not the developer's official list): 1BR+Study from about $1.2M, 2BR from about $1.4M, 2BR Premium from about $1.7M, 3BR from about $2.1M, 3BR Premium from about $2.3M, 4BR from about $2.9M, 4BR Premium from about $3.1M. Implied PSF clusters at $2,300 to $2,570. Official pricing releases at the Sep/Oct 2026 preview.

Which schools are in the 1 km ring? Ai Tong School (P1 first priority). Note: Ai Tong has gone to Phase 2C balloting recently, so 1 km radius improves odds but does not guarantee a seat. Within 1 to 3 km: Catholic High, CHIJ St Nicholas Girls', Raffles Institution, Raffles Girls' Secondary, Marymount Convent, Bishan Park Secondary.

How far is the MRT? Upper Thomson MRT (TE8) is a 1-minute walk via side gate. Bright Hill MRT (TE7) is around 8 to 10 minutes on foot. Bright Hill becomes a CRL plus TEL interchange when CRL Phase 1 opens in 2030, with Phase 2 extending in 2032.

When is TOP? Expected around 2032 pending official confirmation at preview.

Why was the land so cheap? En-bloc redevelopment, not GLS. The Thomson View collective sale took 5 attempts over 17 years. The reserve price was cut from $918M to $808M to get the deal done. Three-way JV (UOL plus Singapore Land plus CapitaLand) de-risked the megaproject scale and enabled aggressive bidding at $1,178 PSF PPR.

Is there a risk of supply oversupply? 1,268 units is megaproject scale, so absorption risk at launch is real. Mitigants: no competing private launches inside 1 km through 2030, strong developer brand with 87% to 99% recent launch absorption, structural RCR scarcity (only 1,269 existing condo units within 500 m), and the cheapest land basis in the 2026 cohort which gives the consortium pricing flexibility.

What is the rental yield estimate? Gross around 3.5% to 3.6% on 2BR or 3BR at mid-scenario pricing. Net 2.4% to 2.6% after expenses. RCR-norm, not best-in-class.

Does Thomson Reserve have an integrated mall? No. It has MRT-linked access to Thomson Plaza (1979 mall, FairPrice, F&B). Some marketing positions this as "integrated lifestyle". The reality is best-in-class connectivity to a nearby mall, not on-site integrated retail like Lentor Modern. Expect 5% to 8% of the integrated-lifestyle rental premium to apply, not the full 13% premium that true integrated developments command.

How does Thomson Reserve compare to Lentor Gardens? Different region (RCR D20 versus OCR D26), 2.5x larger scale (1,268 versus 499 units), longer TOP wait (2032 versus 2030), stronger developer pedigree (3-way blue chip JV versus Kingsford solo), better post-TOP exit liquidity (CRL 2030 plus MacRitchie buffer plus no Plot 2 competition). Lentor Gardens is the better OCR value entry. Thomson Reserve is the better RCR long-hold thesis. Read both if you're shortlisting 2026 launches in the TEL corridor.

Let's talk

If Thomson Reserve is on your shortlist, or you are comparing it against Lentor Gardens, Dover Drive, or the Thomson corridor resale market, drop me a message. I will pull the specific floor plans you are looking at, run the actual numbers against your budget and time horizon, and give you a straight answer. No sales pitch, no rushing the decision. Whether you end up buying here or deciding something else fits your situation better, you walk away with a clearer picture of what you are actually paying for.

If you just want to talk through the numbers without committing to anything, that works too. Most of the people I work with take a few months to make up their mind, and that is the right pace for a $2.5M decision.

WhatsApp +65 8813 0383 · Message me directly

Jet Lim · CEA R072172Z · ERA Realty Network · The ALPHA Framework

Further reading on this site

If you found this review useful, these related pieces extend the analysis with context, comparisons, and tools you can apply to your own shortlist:

- Lentor Gardens Residences Review 2026. The OCR D26 alternative on the same TEL line. Comparable framework, different cycle position and developer pedigree. Useful to read alongside this Thomson Reserve review if you are weighing RCR mispricing (Thomson) against late-cycle OCR value (Lentor).

- Hudson Place Residences Review 2026. The RCR D05 second-mover. Same ALPHA framework, different precinct dynamics.

- Why New Launch PSF is Hitting $3,500 in the RCR. The land cost drivers that explain why Thomson Reserve's $1,178 PSF PPR is a structural anomaly.

- Singapore Property Outlook 2026. The macro frame for District 20 in the cycle.

- The 2026 HDB Upgrading Guide. For Bishan or AMK upgraders pricing a move into the Thomson cluster.

- The ALPHA Framework methodology. The five-pillar lens used in every review.

Disclaimer

This review reflects my professional opinion based on publicly available data and current developer marketing materials at the date of writing (June 2026). It is not financial, investment, or legal advice. Property purchases involve significant financial commitment and risk. Consult a qualified financial advisor, mortgage broker, and conveyancing lawyer before committing.

This is a pre-launch review using the preview-pricing framework. Prices, availability, unit mix, configuration, and project details are subject to change by the developer. Unit counts, sqft ranges, and pricing estimates cited as "EST" are from current marketing materials and are subject to revision at preview. Scenario tables, rental yield estimates, land-to-launch multipliers, and CAGR comparisons are based on publicly available data and are estimates, not guarantees of future performance.

Jet Lim · CEA R072172Z · ERA Realty Network · CEA regulatory notice